Poverty in old age

According to the Federal Statistical Office, 19.4% of people aged 65+ in Germany were at risk of poverty in 2024 – almost one in five people in this age group. For women, the proportion was around three percentage points higher than for men.

A number of factors come together to prevent you from slipping into poverty in old age. In our finance blog, we describe what these are and the reasons why you should start saving for your retirement now.

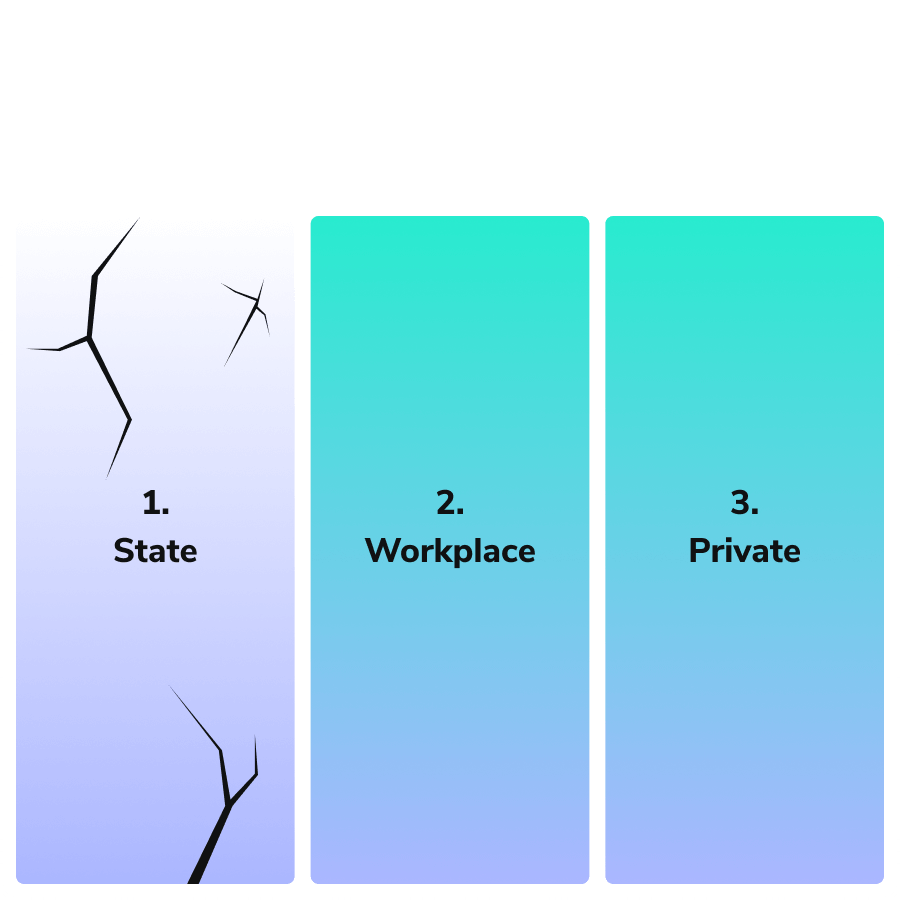

The three pillars of retirement provision

|

State pension = Basis of the retirement pension in Germany |

|

Workplace pension schemes are offered by employers and subsidised by the state as additional security for retirement. |

|

Private pension provision:  Pension insuranceEndowment insuranceHome financing Pension insuranceEndowment insuranceHome financing |

|

It is essential to understand the interplay between the three elements: Because the first pillar - the state pillar - is under strain due to the increasingly ageing population, more emphasis needs to be placed on the other two. |

Service of a good pension scheme

Only the best for elderly people: this motto can only be realised if the right course is set ahead of time. It is particularly important to pay attention to the costs and conditions:

|

The highest possible level of transparency |

|

The right degree of flexibility |

|

Risk/return ratio** according to your investment type and risk tolerance | |

Inheritance treatment |

**Risk and return are two sides of the same coin. An investor must tolerate a certain risk in exchange for the prospect of a return. And it is only in the long term that more risk generally means more return.

Investors differ enormously in terms of their investment horizon and risk tolerance. The pension product must therefore always be in line with the individual's need to continue to sleep well at night. And it must suit the personal financial situation.

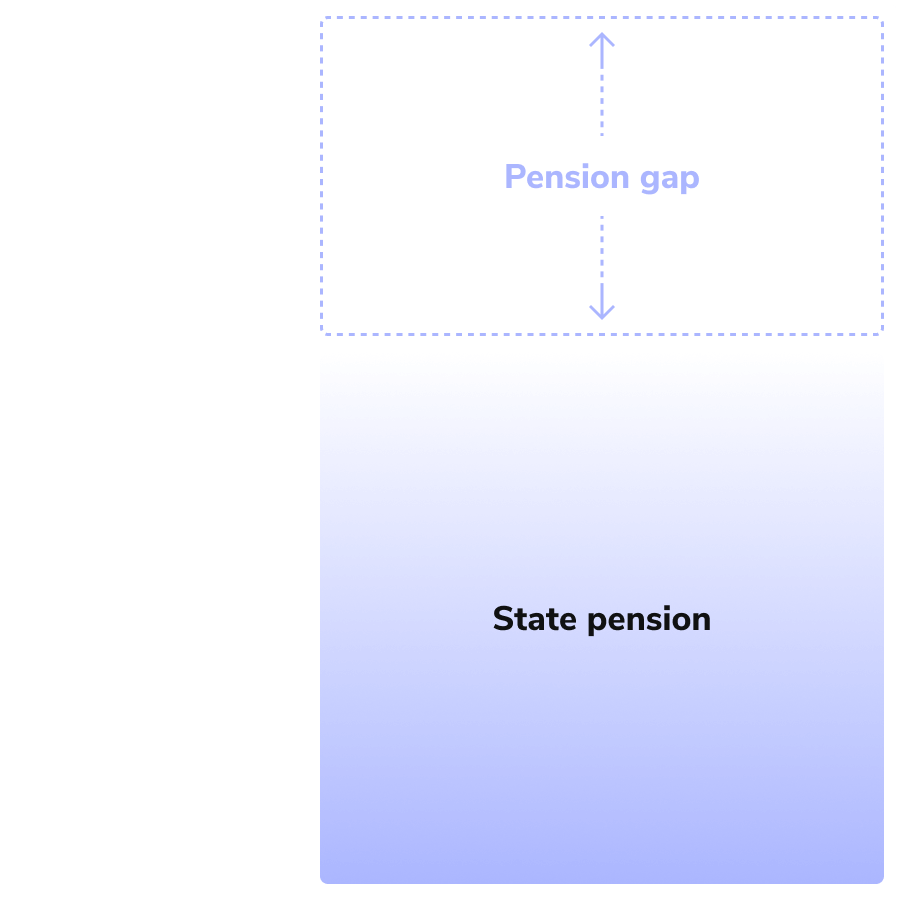

Knowing your own pension gap

How much money is needed for a comfortable retirement

The pension gap is the difference between the amount you need to live on in retirement and the income from your state pension. This gap arises because in most cases the state pension cannot fully cover your expenses as it does not correspond to your full salary. In short: it is the money that is missing from a pension such that it does not achieve the desired standard of living.

The personal pension gap is calculated as simply as that:

Amount of money needed to live on in retirement

|

Know your income from the pension: This information is contained in the pension information on page 1. |

|

Determine outgoings during retirement: Once an overview of current outgoings (rent, insurance, purchases, contracts, etc.) has been obtained, a realistic decision can be made about how much money should be spent each month in retirement. |

|

Take inflation and pension increases into account: It is important to note that the current capital will be worth significantly less in a few years due to inflation. Even if there are regular pension increases to compensate for this, they do not always compensate. |

Note: An exact calculation is not possible as some assumptions are made about the financial future.

|

|

In order to close the pension gap, private provision should be made in addition to the state pension. |

State support for your retirement provision

Private retirement provision will be revolutionised in 2027 by the new retirement provision account.

The federal government is modernising private provision. The new retirement provision account is intended to enable low-cost capital market investments with attractive tax benefits.

Reasons for the reform

- Demographic change: The rising proportion of older people in the population is putting the existing statutory pension system under pressure.

- Low return opportunities: Classic savings models often no longer achieve the required returns for stable provision.

- Transparency and flexibility: The need for transparent and flexible provision products is growing.

Whether you provide for yourself or as an Early Start Pension for children: We accompany your path to a carefree future. As soon as the new retirement provision account is anchored in law, Scalable will provide a corresponding offer. Already today, we offer you the opportunity to provide privately for retirement.