Bits & Pieces

Edition #291 | 07/08/2026

Most traded | Markets & Macro | Weight Loss | Chart of the Week | Healthcare-ETFs | Retirement planning in focus

Go big or go home. That seems to be the motto of the current earnings season. Both in the US and domestically, record results have catapulted benchmark indices to new all-time highs. In the spotlight this week: healthcare players. Taking center stage are weight-loss pioneers Eli Lilly and Novo Nordisk. But even beyond the fat burners, the healthcare sector is offering hefty returns. Plus, we take a close look at the individual sectors within the S&P 500 and STOXX 600.

Note: The data refers to the ratio of purchases and sales of the 100 most traded stocks on Scalable Broker between 31/07/2026 and 06/08/2026.

In the spotlight

A few weeks ago, SAP shares fell to a 52-week low. The reason is simple. A lowered profit forecast ahead of its Q2 results as well as expensive AI acquisitions. Since then, the DAX-listed group has regained ground. After all, the results were anything but bad: earnings per share logged a 30% increase compared to the previous year.

Summer of records

So much for the summer slump. On August 4th, the DAX climbed to a new record high of over 26,200 points. Falling oil prices and (renewed) glimmers of hope for an end to the Iran conflict brought summer cheer. Additional momentum came from the ongoing earnings season, which is brimming with lavish profits. Siemens, for instance, reported record order intake and raised its outlook. Same same, but different at its Munich neighbor Siemens Energy. Chip manufacturer Infineon also delivered, though its stock slipped anyway as investors penalized a slight margin miss.

The S&P 500 likewise climbed to a new high - according to FactSet, around 90% of the companies in the benchmark index reported earnings per share (EPS) above expectations. That includes NVIDIA rival AMD. However, following a 50% revenue jump in the second quarter, investors had expected an even higher forecast for the subsequent quarter. SpaceX, too, lost further ground despite strong numbers, weighted down by multi-billion-dollar AI investments.

Whether the rally runs out of steam is also up to the US Federal Reserve. The upcoming labor market report serves as a gauge for future monetary policy, determining how much breathing room the Fed has at its next meeting in September, having recently kept interest rates at 3.50% to 3.75%.

Slim-down showdown

If there were a word of the year in the pharma industry, weight-loss injections would have undoubtedly claimed the title multiple times over. Zepbound and Wegovy have already poured billions into the coffers of their creators, Eli Lilly and Novo Nordisk. Both rivals are looking toward a massive future: the market for obesity and diabetes medications in the US alone—the world's highest-revenue healthcare market—is projected to head toward a volume of over $100 billion by 2030. So now the question: Lilly or Novo?

- US Top Dog: In the showdown with Novo, Lilly holds a clear lead. This is due not only to its more sought-after weight-loss treatments, but also to a broader product portfolio that includes cancer and Alzheimer’s therapies. The US home-field advantage provides an additional tailwind, free of trade barriers. The numbers underline this success: a 48% increase in Q2 revenue significantly beat expectations, with Zepbound acting as a key driver. Lilly raised its full-year guidance.

- Turnaround Candidate: Although Novo is considered the pioneer of weight-loss injections and specializes in diabetes and obesity drugs, the Danish firm has been on a downward trend for some time. Clinical trials failed, production bottlenecks weighed heavily, and additionally the bitter competition from Lilly. Recent numbers are mixed: while Novo now anticipates less currency-adjusted revenue loss for full-year 2026 than previously projected (0 % to -6 % instead of -4 % to -12 %), sales of its Wegovy pill disappointed investors.

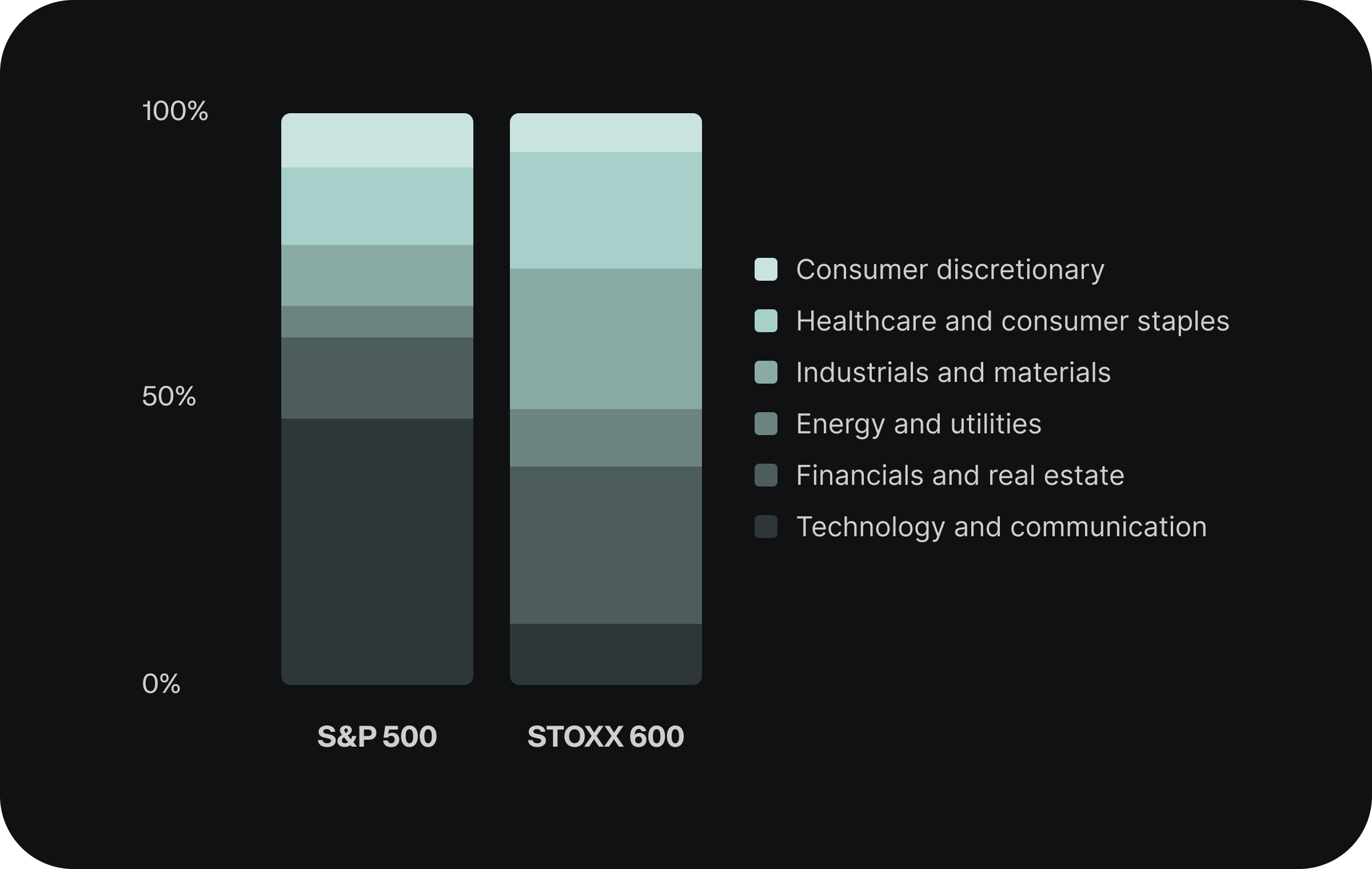

Opposites attract returns

Sector weighting comparison: S&P 500 vs. STOXX 600

Source: S&P Global, STOXX, as of July 31, 2026

When you buy the S&P 500, you are adding the driving forces of the US economy to your portfolio—and those are primarily tech stocks. Unsurprisingly, the two tech sectors (IT and Communication) together account for roughly 46% of the index weight. Actual tech exposure is likely even higher. Sector assignment can be tricky, as seen with Amazon: due to its e-commerce revenue, the cloud giant is officially still classified under "Consumer Discretionary," driving that sector's heavy weighting in the S&P 500.

With so much tech, a counterweight is needed to ensure proper portfolio diversification. The STOXX 600 could be the ideal solution. The index tracks the performance of the 600 largest listed companies across 17 European countries, free of major cluster risks. Technology and Telecommunications (the sector carries a slightly different name here) account for just under 11%, while Financials and Real Estate claim 26%. Industrials and Basic Materials account for a 24% weighting.

A quantum of health

The multi-billion-dollar battle over fat-burners is big. But as the saying goes: Think bigger. The overall healthcare sector is bursting with innovation, from mRNA and biotech to surgical robotics. With Healthcare ETFs, you bet on a multitude of megatrends in a market with guaranteed demand—because people always get sick. A word of caution: healthcare is not immune to pullbacks either.

With the Xtrackers MSCI World Health Care ETF, you can add more than 100 healthcare players to your portfolio. However, nearly 70% of the ETF’s volume is concentrated in the US, with Eli Lilly as its top position. To reduce cluster risk, you can blend in the Amundi STOXX Europe 600 Healthcare ETF. Alongside European pharma giants such as Novartis, AstraZeneca, Roche, and Novo Nordisk (accounting for around 50% of the ETF), it invests in laboratory and medical technology as well as healthcare management.

For tech enthusiasts, the iShares Healthcare Innovation ETF is a strong option. It only lists companies that generate a significant portion of their revenue in innovative fields such as genetic engineering, immunotherapy, or surgical robotics.

Product-Highlight

ADVERTISEMENT

Data Center riches

Artificial intelligence has a gargantuan appetite for power. The International Energy Agency predicts that the global annual electricity demand of data centers could double to around 900 to 1,000 terawatt-hours (TWh) by 2030. For comparison: Germany’s entire electricity consumption in 2025 stood at 526 TWh.

If you’ve developed an appetite for energy play, you can add the Xtrackers Electrification Technologies & Smart Grid UCITS ETF to your portfolio. The ETF targets companies working on smart grid infrastructure and electrical technology. Top holdings include DAX heavyweights like Siemens Energy and the US power and thermal engineering supplier Honeywell Technologies, which we covered in the last issue of "Bits & Pieces."

While the Magnificent 7 have to justify their massive AI capital expenditures, power utilities and equipment providers are rubbing their hands in glee. Instead of taking on single-stock risk, this ETF lets you add the entire energy fleet to your portfolio in one move.

The world x2

With the Scalable MSCI AC World Leveraged Daily Swap Xtrackers ETF, there is now the first 2x leveraged world ETF providing access to more than 2,400 stocks across 47 developed and emerging markets. Additionally, with a total expense ratio (TER) of 0.45% p.a., it is the most affordable broadly diversified leveraged ETF in Europe. The leverage effect doubles daily market movements, amplifying gains and losses alike.

1% Bonus on private equity

For a short time, Scalable is topping up your invested amount in the BlackRock Private Equity Fund by 1%. Terms and conditions apply. This makes an already exciting alternative to the stock market even more attractive: getting in on promising companies before they take the leap to go public.

The BlackRock Private Equity Fund lets you capitalize on this opportunity. The most recognizable names in its current 14-company portfolio are likely OpenAI and Anthropic—these AI pioneers act as the venture seasoning. Meanwhile, the focus remains on established platform, industrial, and consumer goods companies such as Vinted, Stepstone, Carglass (Belron), or Froneri (ice cream). The major advantage: through the co-investment model, retail investors invest in the exact same deals as institutional players.

Investments involve risks. Liquidity restrictions apply. Please review the specific product information.

In this section, we answer your most important questions about the Retirement Investment Account (AVD).

How should one divide investments between a Retirement Savings Account (AVD) and a standard ETF portfolio in percentage terms?

No blanket statement can be made here, as it depends heavily on individual factors. Here are three key points to consider when deciding:

- The Subsidy Base (AVD): State subsidies are available up to a personal contribution of €1,800 per year. Because you receive up to €540 in allowances on top (representing a whopping 30% instant return), it is often wise to max out this amount in the AVD first.

- Purpose vs. Freedom: The AVD is primarily a "one-way street" aimed at retirement. Assets can only be withdrawn without forfeiting subsidies in very select cases (e.g., home building or renovation). If you need funds for medium-term goals (an emergency fund, a trip around the world), you should keep that money in a standard portfolio, where you maintain flexibility and instant access.

- Tax Check: In the AVD, you frequently benefit from deferred taxation, which can be advantageous—meaning you pay no taxes during the accumulation phase. In a standard portfolio, you pay capital gains tax on profits.

Editorial deadline: Friday, 7 a.m.

Sources: Scalable and dpa-AFX